Are the finance and insurance companies in the last-chance saloon to salvage their future?

Technology has, and always will disrupt, the status quo for individuals and corporates alike. The last few years have seen industry-specific tech platforms create upheavals – key examples being FinTech, InsurTech, EdTech/EduTech and HRTech. A number of established players in each of these industries have been working aggressively to update their products and services portfolio to adapt and leverage these technology platforms. Kudos to them.

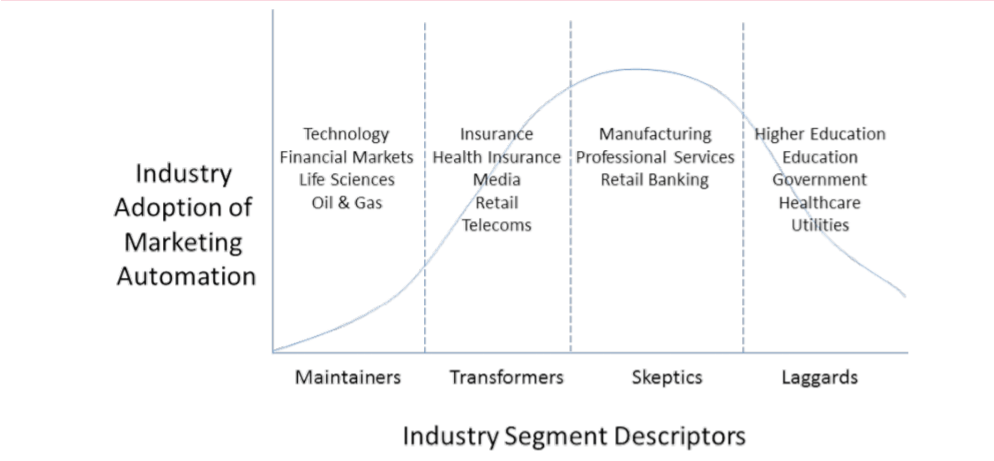

Second paragraph should be: However, in this process, they have become laggards in the adoption of MarTech and AdTech platforms. A 2014 Ovum study had identified Banking and Insurance as being laggards in terms of their adoption of Marketing Automation Platform.

A 2017 industry study showed that their adoption of MAP had dropped further and now they accounted for less than 10% of MAP installations.

What this implies is that in the banking and insurance industry, the customer experience that they can provide is broken at best and dysfunctional at worst.

Established banks and insurance companies are working hard to leverage and adopt BlockChain and FinTech to update their products and services. However, as customers, we still receive multiple communications, which are not personalized and don’t understand our specific requirements, forget predicting them. This poor customer experience means that customers are finding it easier to adopt digital native start-ups like TransferWise, rather than wait for the established banks to update their digital experience.

What banks need to understand is that customers, be it as an individual customer or a corporate customer, are used to a digital-first (but omni-channel), mobile-friendly, seamless customer experience in all their interactions. They expect, nay demand, the same level of experience when they interact with the FSI institutions and will very quickly look for alternatives if the experience is sub-optimal

In this aspect, these companies need to take a lot of inspiration from High-tech companies. These companies were considered also-rans in terms of their marketing activities, with marketing teams being seen as event organizers and brochure printing departments. However, through an aggressive adoption of MarTech and AdTech, they have managed to get a table at the board, have rebranded themselves as revenue generators and not cost centers, and are now leading the charge in terms of innovation in B2B marketing practices.

It is a wake-up call for all the marketers in the banking and financial industry that they could very well be left behind if they do not transform their experience delivery processes and mechanisms to match up with what customers now regard as a must-have. The best or products and services will not entice me to use them unless the experience itself is good.

What makes it easier for them, though, is that there are ample learnings and best practices available from these early adopters that can help them jump start this process. Similarly, there are agencies, like Verticurl, that can help you in this change management and tech adoption process. However, if you miss the boat, there may no longer be any customers left for you to engage.

Here are a few use cases based on Verticurl’s 10+years of experience of helping other companies get started and excel:

-

Enable your relationship marketers (RM’s) to send a thank you note to their Small and Medium Banking customers immediately after they have met at an event aimed at educating them on Trade Financing. This will not only help them engage their customers much better but also enable the bank to capture all relevant interaction data

-

Run an automated onboarding program for all Commercial Banking customers to help them understand the features and functionalities available to them online, by integrating your Marketing Automation Platform with your transactions system.

-

Provide your RMs with dashboards and triggers based on engagement activities of contacts from their priority key accounts, enabling the RMs to have more relevant conversations.

-

Personalize the mobile app experience of corporates with relevant information, e.g. all Small and Medium Banking customers with investment in the UK market should have a link to your analyst papers about Brexit.

-

Track form abandonment for self-serve products like Corporate Credit Cards and run remarketing campaigns or outbound calls from tele-agents to help them complete the applications.